If you are tracking the Tata Motors share price today, you might notice something different compared to a few years ago. Following the historic demerger in late 2025, investors now watch two distinct entities: Tata Motors Passenger Vehicles (TMPV) and Tata Motors Commercial Vehicles (TMCV).

As of early February 2026, both stocks are in the spotlight following the release of their Q3 (October-December 2025) financial results. While revenue numbers are strong, profit figures have seen a dip due to one-time costs, leaving many retail investors wondering: is this a buying opportunity or a time to wait? Here is a simple breakdown of what is happening with Tata Motors shares.

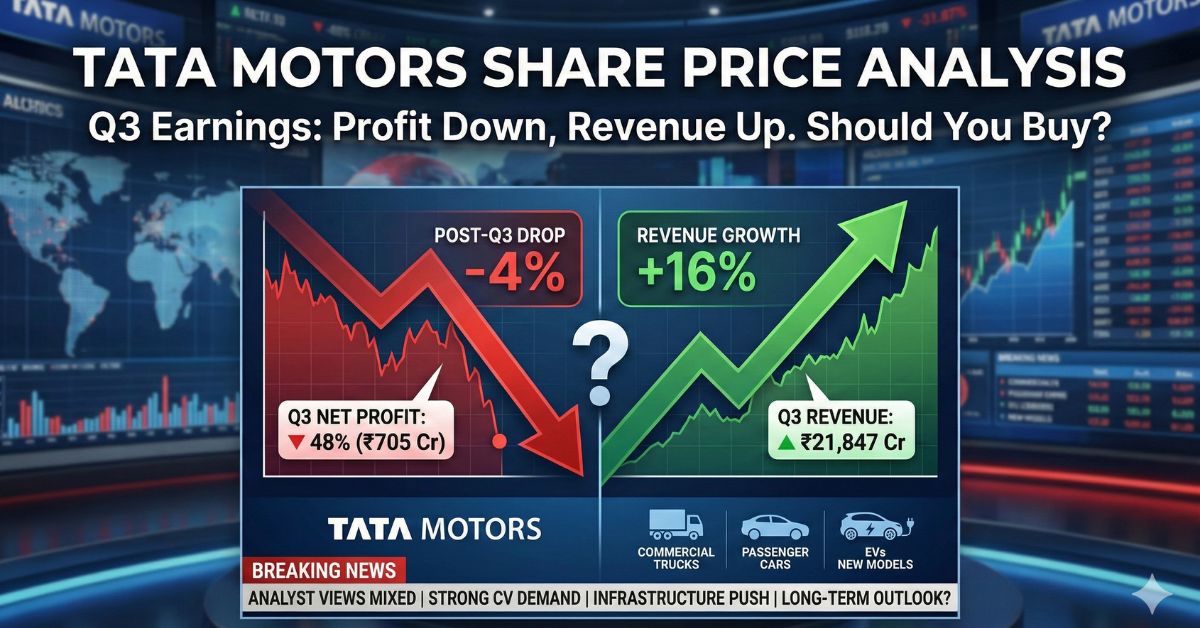

What Happened: Q3 Earnings Analysis

The biggest trigger for the current share price movement is the recent Q3 earnings report released in late January 2026. The results presented a mixed picture for investors.

1. Commercial Vehicles (TMCV)

The Commercial Vehicle arm, often considered the backbone of the group, reported a 16% rise in revenue, reaching approximately ₹21,732 crore. This growth was driven by high demand for trucks and buses, aided by the government’s continued infrastructure push.

However, the net profit dropped by nearly 48% to ₹705 crore.

- Why the drop? This wasn’t due to bad business. The company paid significant “exceptional items” (one-time costs) related to the recent demerger and adjustments for new labor codes.

- The Good News: The operating margin (EBITDA) remained healthy at around 12.7%, showing that the core business is actually very profitable.

2. Passenger Vehicles (TMPV)

The Passenger Vehicle stock (covering cars, SUVs, and EVs) has seen some volatility. The company recorded its highest-ever annual sales in 2025, crossing 5.8 lakh units. However, the stock recently faced mild pressure due to fears surrounding the India-EU Free Trade Agreement, which could lower import taxes on European luxury cars, potentially increasing competition.

Why It Matters: The “Exceptional” Cost Factor

For a common investor, a “48% profit drop” sounds scary. But experts suggest looking deeper.

When a company spends money on “exceptional items” like restructuring or legal changes, it is usually a one-time expense. It does not mean the company is selling fewer cars or trucks. In fact, Tata Motors’ core sales volumes are up.

- CV Sales: Up by 20% year-on-year.

- EV Dominance: Tata continues to hold over 70% of India’s electric vehicle market share.

This suggests that the foundational business is strong, even if the headline profit number looks lower this quarter.

Background: The Demerger Explained

If you have been away from the market for a while, remember that Tata Motors completed a major split (demerger) in late 2025.

- Entity A (TMCV): Focuses on trucks, buses, and heavy machinery. It is linked to India’s economic growth and infrastructure (roads, mining, construction).

- Entity B (TMPV): Focuses on cars, SUVs (Nexon, Harrier, Punch), and Electric Vehicles. It is linked to consumer spending and lifestyle.

This split allows each company to focus on its own strengths. Currently, the market is valuing them separately, which is why you see two different share prices reacting differently to news.

Impact on Investors

- Short Term: The stock might remain choppy (moving up and down slightly) as the market digests the Q3 profit numbers and the India-EU trade news.

- Long Term: Brokerages like ICICI Securities and Nomura have maintained positive ratings (like ‘Add’ or ‘Buy’) for the Commercial Vehicle unit. They believe the government’s spending on highways will keep demand for Tata trucks high.

What Happens Next?

Investors should watch out for the following in February 2026:

- Management Commentary: Further updates from the CEO on how the new labor codes will impact costs in Q4.

- EV Sales Data: Monthly sales numbers for the Passenger Vehicle unit to see if they can maintain their lead against competitors like Mahindra and Maruti.

- Global Markets: Any recovery in the JLR (Jaguar Land Rover) global sales, which supports the group’s overall revenue.

Read More : Stop Lugging Your Engine

Frequently Asked Questions (FAQs)

1. Why are there two Tata Motors stocks now?

Tata Motors split its business into two separate listed companies in late 2025: one for Commercial Vehicles (trucks/buses) and one for Passenger Vehicles (cars/EVs). This was done to let each business focus on its specific growth strategy.

2. Is Tata Motors share price falling?

The Commercial Vehicle (CV) stock saw a slight dip recently because their reported profit fell due to one-time costs. However, their sales (revenue) actually went up. The stock is not crashing; it is adjusting to these result numbers.

3. Is Tata Motors a good buy for the long term?

Most market experts remain positive. The Commercial Vehicle business is strong due to India’s infrastructure growth, and the Passenger Vehicle business is the leader in the Electric Vehicle (EV) sector.

4. What is the main risk for Tata Motors right now?

For the passenger car business, the main risk is increasing competition from foreign brands if import taxes are lowered (India-EU deal). For commercial vehicles, the risk is any slowdown in government construction projects.

5. Did Tata Motors declare a dividend in Q3 2026?

No specific dividend was declared in the Q3 results. Dividends are typically announced closer to the end of the financial year (March/April).